Petron Malaysia Refining & Marketing Bhd (KL:PETRONM) delivered a strong performance for the third quarter ended September 30, 2025 (3Q FY2025), securing a substantial profit turnaround driven by operational efficiencies and refinery optimization, successfully mitigating the persistent impact of declining global oil prices. The results underscore the company’s focus on effective resource management and risk mitigation strategies.

I. Financial Performance: The Profit Turnaround

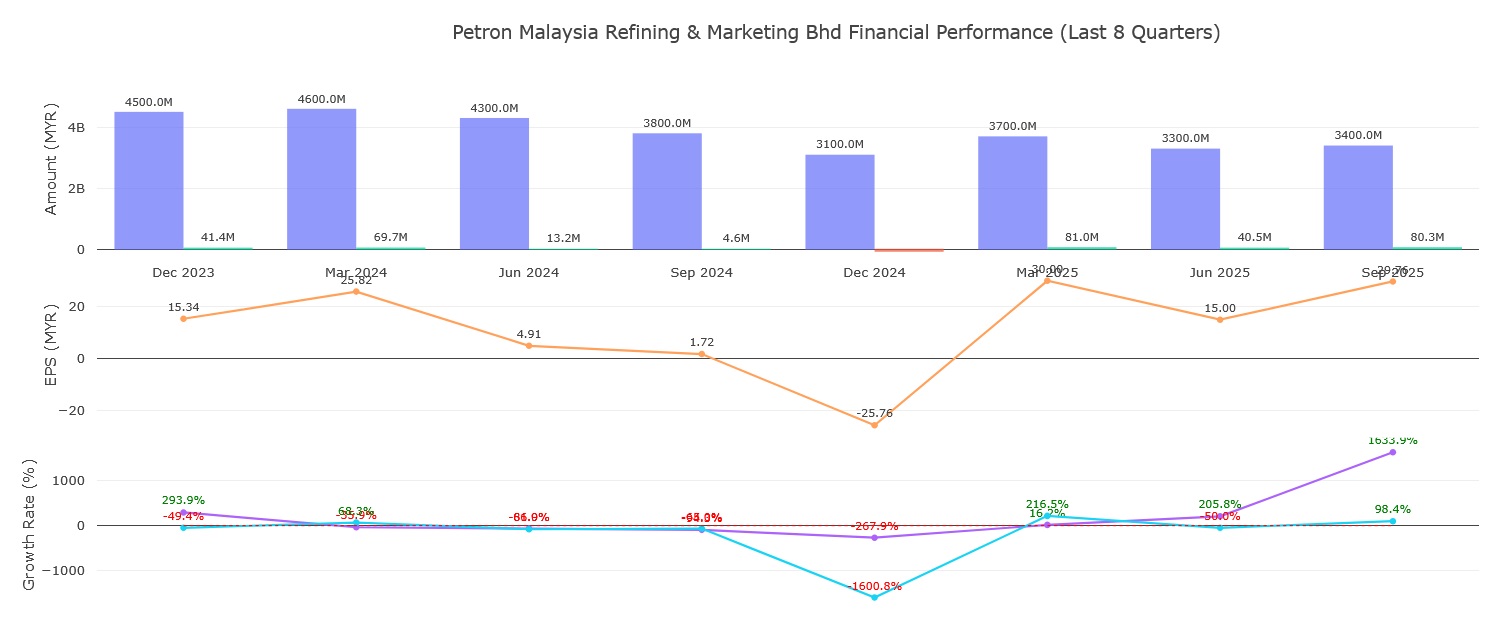

Petron Malaysia’s Q3 FY2025 was marked by a dramatic surge in profitability, although revenue declined due to lower commodity prices.

| Metric | Q3 FY2025 (MYR’000) | Q3 FY2024 (MYR’000) | Variance (YoY) | YTD FY2025 (MYR’000) | YTD FY2024 (MYR’000) | YTD Variance (YoY) |

| Revenue | 3,410,183 | 3,814,541 | -10.6% | 10,343,195 | 12,756,064 | -19.0% |

| Profit Before Tax | 111,548 | 7,394 | >1000% | 275,843 | 110,529 | +149.6% |

| Net Profit (PAT) | 80,347 | 4,634 | >1000% | 201,884 | 87,587 | +130.5% |

| Basic EPS (sen) | 29.76 | 1.72 | N/A | 74.77 | 32.44 | N/A |

Key Financial Insights:

1. Record Quarterly Profit Surge: Net profit attributable to shareholders jumped to RM80.347 million in 3Q FY2025, a massive increase compared to RM4.634 million in the corresponding period last year. The resulting operating income of RM138,661 thousand was a significant turnaround from the operating loss of RM15,886 thousand incurred in 3Q FY2024.

2. YTD Profit Doubling: For the first nine months of FY2025, the company delivered a net profit of RM201.884 million, growing more than twice compared to the RM87.587 million achieved in the same period last year.

3. Revenue Decline Tempered by Volume: Quarterly revenue shed 11% (to RM3.41 billion) and YTD revenue decreased about 19% (to RM10.34 billion). This decline was mainly due to declining crude oil prices, which averaged US69 per barrel in Q3, 80 in 3Q FY2024. However, this price impact was partly tempered by higher sales volume.

II. Operational Deep Dive: The PD Refinery Advantage

The group’s strong earnings are overwhelmingly attributed to its operational prowess, particularly the efficiency of its refinery and its strategic response to market volatility.

• Refinery Optimization as Key Driver: The improvement in Q3 net profit was mainly driven by the sustained process optimisations and higher utilization of the Port Dickson (PD) Refinery. This optimization led to improved plant utilization and an increased production of higher-value refined products.

• Higher-Margin Product Mix: The sustained optimized refinery production yielded more higher-margin gasoline and diesel while reducing the exports of low-margin by-products.

• Sales Volume Growth: The company sold 9.4 million barrels for the first nine months of 2025, a 2% increase compared to 9.2 million barrels in the prior year. This was supported by a 4% growth in domestic sales volume, even though exports decreased by 1%.

• Risk Management: Prudent hedging strategy and working capital management were key factors that mitigated the impact of the challenging market conditions. Furthermore, the improved earnings for the first half of FY2025 were also attributed to focused efforts to reduce financing costs and commodity price exposures through effective risk management strategies.

III. Financial Health and Efficiency Metrics

Analysis of PETRONM’s financial health reveals momentum in capital returns and strong cash flow quality.

• Improving Returns on Capital Employed (ROCE): PETRONM’s ROCE was 2.7% based on the trailing twelve months to June 2025. While this is lower than the Oil and Gas industry average of 9.0%, the ROCE trend is positive. The company was generating losses five years ago but is now earning 2.7%, indicating that prior investments are paying off. The company is also employing 62% more capital than previously, suggesting continued reinvestment opportunities that generate higher returns.

• Strong Free Cash Flow (FCF): The company’s earnings quality appears strong, indicated by a solid accrual ratio of -0.12 for the year to June 2025. A negative accrual ratio is generally viewed positively, meaning that the company’s statutory earnings were quite a lot less than its free cash flow (FCF). The company reported FCF of RM356 million in the last twelve months, which was well over the RM56.6 million reported profit, suggesting the earnings potential is “at least as good as it seems, and maybe even better”.

• Net Asset Value: The net assets per share attributable to ordinary equity holders of the parent increased to 9.4317 as at the end of the current quarter, up from 8.7592 at the preceding financial year end.

IV. Outlook and Growth Momentum

The company is focused on strategic expansion, sustainability efforts, and maintaining operational efficiencies to sustain its performance.

1. Sustainability Projects: Petron Malaysia is “halfway through” the construction of its second palm methyl ester (PME) biodiesel plant. This plant aims to boost the company’s capability to produce biodiesel blended with sustainable PME.

2. Market Expansion: The company has continued to expand its retail reach, having streamed 15 new service stations under the Petron Malaysia group. The company remains committed to strengthening operations, expanding market reach, and delivering long-term value.

3. Mitigation of Volatility: The management emphasizes that its capabilities to enhance operational efficiencies, manage resources effectively, and mitigate business risks remain crucial in sustaining strong performance amid ongoing market volatility.

V. Investor Insights

• Earnings Quality: The strong negative accrual ratio suggests that shareholders, who appeared unconcerned with the Q2 (lackluster) earnings report, may have reason for hope, as the underlying free cash flow indicates the earnings are stronger than they seem.

• Growth Potential: The momentum in ROCE, coupled with the business employing more capital, suggests the company has potential reinvestment opportunities. This signals that investors may not be fully aware of the promising trends yet.

——————————————————————————–

Actionable Takeaway:

Petron Malaysia’s Q3 results demonstrate successful internal strategies (refinery optimization, prudent hedging) enabling massive profit growth despite a global downturn in oil prices that suppressed overall revenue. For investors, the strong operational execution leading to higher-margin products and the robust Free Cash Flow signaled by the negative accrual ratio suggest underlying financial strength and potential for long-term growth, even as the company works to raise its overall ROCE to industry average levels.

A good way to view the Q3 performance is like a chef who, facing a reduction in the price of their raw ingredients (lower crude oil prices) and thus lower total ticket sales (revenue), successfully upgraded their kitchen equipment and techniques (Port Dickson optimization) to create significantly higher-margin dishes (gasoline and diesel), leading to a much larger profit margin and operating surplus.

Verdict

- Short to Medium Term (3–5 years): We think Petron Malaysia could be a reasonable play if you believe they can keep optimizing their refinery, manage cost exposures well, and maintain decent cash flow. It’s not a very exciting growth story, but more of a value / cash-flow business with some risk mitigation.

- Long Term (10+ years): More uncertain. The EV transition is a big wildcard. If EV adoption accelerates strongly in Malaysia or the region, demand for refined products could decline. That said, if they diversify into biofuels (like with the PME plant) or other downstream products, they might adapt.

- As a Dividend Stock: It’s somewhat moderate yield, but not the most stable dividend champion given earnings risk. If you want income + some growth potential, it’s okay, but not a sure “dividend fortress.”

Disclaimer: This is a technical analysis based on historical price and volume data. It does not constitute financial advice. Always conduct your own research and consider your risk tolerance before making any investment decisions.